🌅 Morning Market Report – Friday, October 10, 2025

Key Takeaway: Global markets open on a cautious note after a mixed close, with most major indices in the red. Gold retreats below $4,000/oz, silver remains strong, and energy prices soften. Investors are digesting softer US inflation data, ongoing trade tensions, and a wave of corporate news. Volatility and defensive positioning are likely to persist.

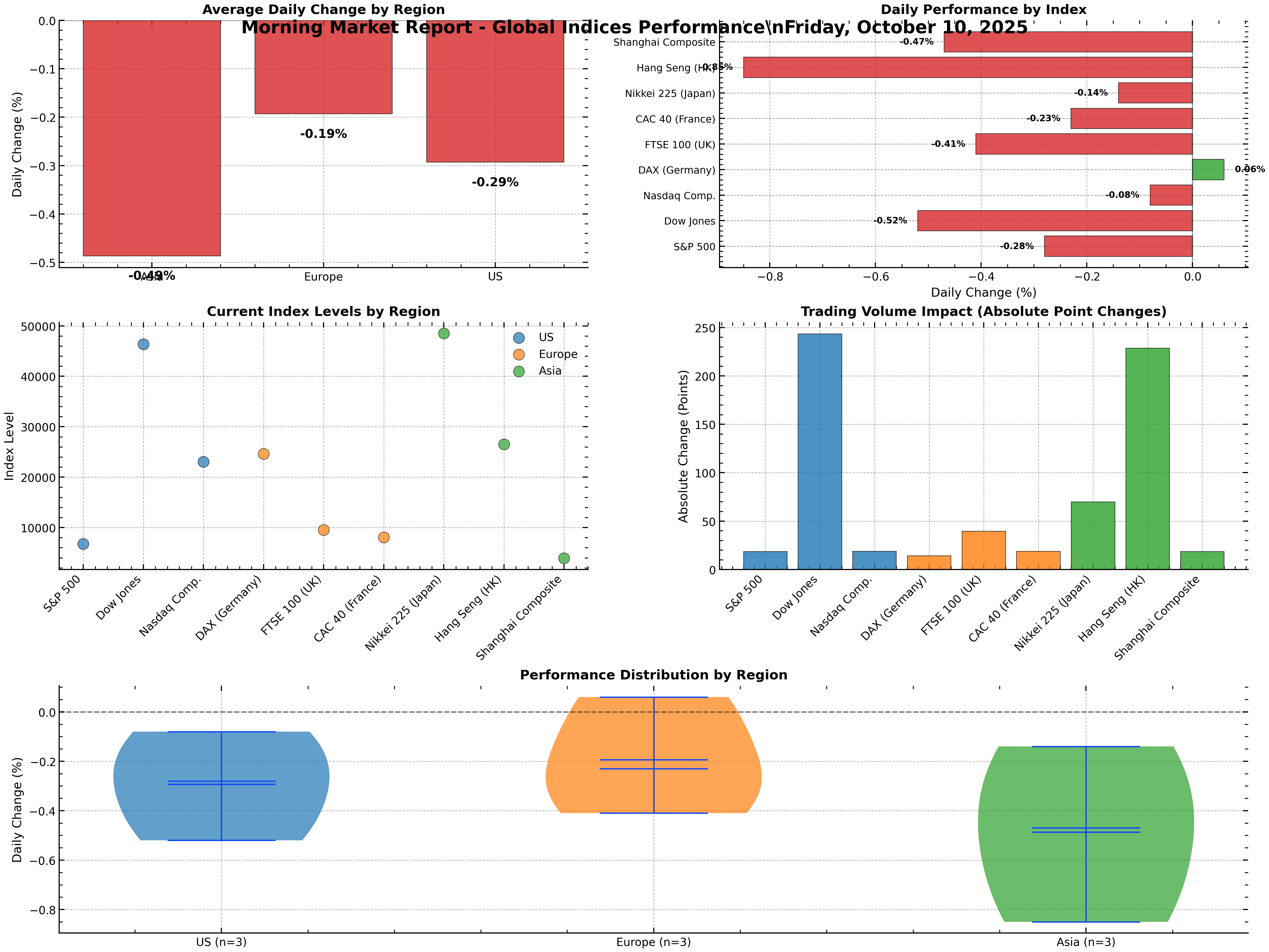

🗺️ Global Market Overview

Index

Last Close

Change (Points)

Change (%)

Region

S&P 500

6,735.11

-18.61

-0.28%

US

Dow Jones

46,358.42

-243.36

-0.52%

US

Nasdaq Comp.

23,024.63

-18.75

-0.08%

US

DAX (Germany)

24,611.25

+14.12

+0.06%

Europe

FTSE 100 (UK)

9,509.40

-39.47

-0.41%

Europe

CAC 40 (France)

8,041.36

-18.77

-0.23%

Europe

Nikkei 225 (Japan)

48,510.72

-69.72

-0.14%

Asia

Hang Seng (HK)

26,523.89

-228.70

-0.85%

Asia

Shanghai Composite

3,915.48

-18.49

-0.47%

Asia

Best performer: DAX (Germany) +0.06% Worst performer: Hang Seng (HK) -0.85% Market breadth: 1 index up, 8 indices down

📊 Visual: Global Market Performance

Figure: Comprehensive global index performance and regional breakdown, October 10, 2025.

💹 Commodities, Currencies & Bonds

Precious Metals

Commodity

Price (USD)

Change (%)

Gold

3,965.01

-0.28

Silver

50.43

+2.63

Platinum

1,609.00

-0.83

Palladium

1,400.50

-1.02

Energy

Commodity

Price (USD)

Change (%)

Brent Oil

64.88

-0.54

WTI Oil

61.23

-0.47

Nat. Gas

3.21

-0.93

Currencies

Pair

Rate

EUR/USD

0.8639

GBP/USD

0.7523

USD/JPY

152.86

USD/CNY

7.1253

Bonds

Country

10Y Yield (%)

US

4.13

Germany

2.70

UK

4.75

Japan

1.69

🏦 Key Market Drivers & Overnight Developments

US Tech & AI: Nasdaq and S&P 500 closed lower, but tech remains resilient. Broadcom, Nvidia, and Super Micro Computer continue to lead after strong earnings and AI optimism.

Inflation & Fed: Softer US producer price data and unchanged Fed rates have increased expectations for a rate cut later this year.

Trade Tensions: EU tariffs on Chinese EVs weigh on European and Chinese stocks, raising global trade concerns.

Commodities: Gold pulls back below $4,000/oz, silver surges to $50/oz+, and oil prices soften as geopolitical tensions ease.

Currency Moves: The US dollar remains strong, especially against the yen and euro.

📰 Major Corporate & Economic News

Tesla: Shareholders approved Elon Musk’s $56B pay package and legal move to Texas; Model 3 price hike in Europe expected.

Broadcom: Raised AI chip revenue forecast and announced a 10-for-1 stock split.

Illumina: Board approved GRAIL spin-off; distribution set for June 13.

GameStop: Annual meeting postponed due to technical issues.

📈 Regional & Sector Insights

US: All major indices down; tech outperformed, but only Consumer Non-Durables sector finished positive.

Europe: DAX eked out a gain; FTSE 100 and CAC 40 declined.

Asia: Nikkei 225 slightly lower after a record run; Hang Seng and Shanghai Composite underperformed.

🧭 Outlook & What to Watch

Volatility likely to persist as investors await more economic data and earnings.

Precious metals may remain in focus amid safe-haven demand and supply constraints.

Key events ahead:

US and European earnings releases

Fed commentary and bond market moves

Geopolitical headlines and commodity swings

🏁 Summary

Markets open with a defensive tone after a mixed close. Gold and silver remain in focus, energy prices are soft, and tech continues to drive sentiment. Stay alert for volatility and sector rotation opportunities as the day unfolds.