Key Takeaway: Global markets are starting Friday with a cautiously bullish tone, led by strong gains in Asia (especially China), a resilient S&P 500, and a firm US dollar. All eyes are on the Federal Reserve’s Jackson Hole symposium, where Chair Powell’s speech could set the tone for the next phase of monetary policy. Commodities are mixed, with gold consolidating near highs and oil holding steady. New US tariffs and persistent inflation are adding complexity to the outlook.

📊 Market Snapshot: Current Prices & Overnight Moves

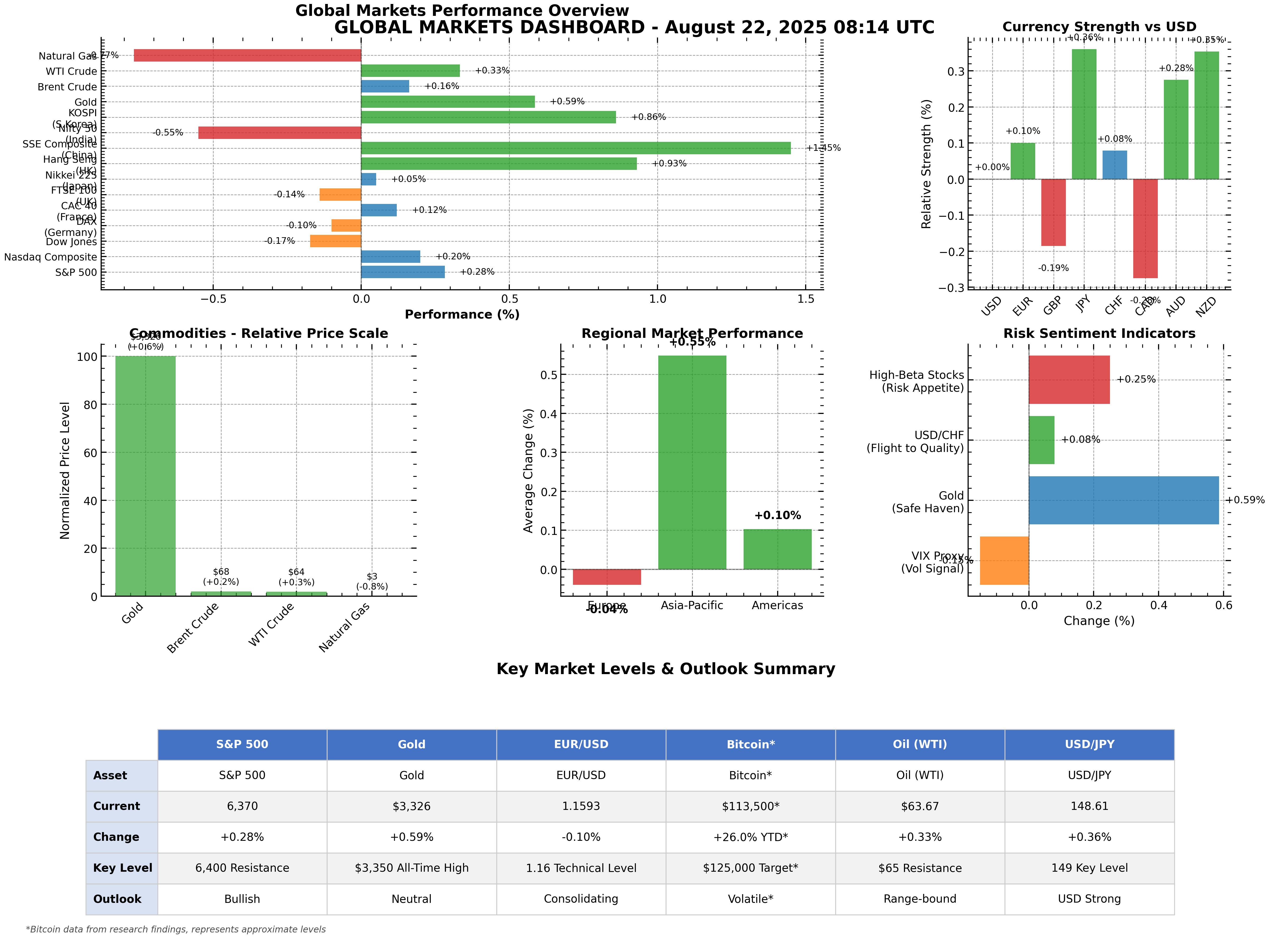

Asset/Class

Current Price

Overnight Change (%)

S&P 500

6,370.17

+0.28%

Nasdaq Composite

21,100.31

+0.20%

Dow Jones

44,785.50

-0.17%

Gold

$3,326.10/oz

+0.59%

Brent Oil

$67.77/bbl

+0.16%

WTI Oil

$63.67/bbl

+0.33%

Natural Gas

$2.78/MMBtu

-0.77%

EUR/USD

1.1593

-0.10%

USD/JPY

148.61

+0.36%

GBP/USD

1.3396

+0.19%

International Indices

Index (Region)

Latest Price

Daily Change (%)

DAX (Germany)

24,268.67

-0.10%

CAC 40 (France)

7,947.89

+0.12%

FTSE 100 (UK)

9,295.83

-0.14%

Nikkei 225 (Japan)

42,633.24

+0.05%

Hang Seng (Hong Kong)

25,339.14

+0.93%

SSE Composite (China)

3,825.76

+1.45%

Nifty 50 (India)

24,946.25

-0.55%

KOSPI (S. Korea)

3,168.73

+0.86%

Figure: Global Markets Dashboard – Performance, Currency Strength, Commodities, and Key Levels (Aug 22, 2025)

📰 Major Market Drivers

Federal Reserve in Focus: Markets are bracing for Chair Powell’s speech at Jackson Hole today. While bond markets still price in a September rate cut, recent Fed commentary has been more hawkish, fueling volatility and uncertainty .

Inflation & Economic Data: US CPI held steady at 2.7% YoY, but PPI jumped to 3.3% (a 5-month high), signaling persistent cost pressures. Retail sales growth slowed, and consumer sentiment weakened, with inflation expectations ticking higher .

Trade & Tariffs: The US imposed new tariffs on hundreds of imports, prompting price hikes from major retailers. This is expected to boost government revenue but could weigh on consumer spending and corporate margins .

Sector Rotation: Small-cap stocks and energy/healthcare sectors are outperforming, while consumer discretionary and homebuilders lag due to higher rates .

Asia Leads, Europe Mixed: Chinese and Hong Kong equities are the day’s top performers, while European indices are slightly lower. The US dollar is firm, especially against the yen and commodity currencies.

🏆 Top Movers & Laggards

Top Performers

Change (%)

SSE Composite (China)

+1.45%

Hang Seng (Hong Kong)

+0.93%

KOSPI (S. Korea)

+0.86%

Underperformers

Change (%)

Dow Jones (US)

-0.17%

Nifty 50 (India)

-0.55%

Natural Gas

-0.77%

💡 Trading Insights & Risk Management

Sentiment: 67% of tracked assets are higher overnight—risk-on mood, but with caution ahead of the Fed.

Opportunities: Asia-Pacific equities (especially China) are showing momentum. Gold is consolidating near highs, and USD/JPY strength may continue if the dollar remains bid.

Risks: Fed policy surprises, tariff impacts, and weakening consumer sentiment could trigger volatility.

Technical Levels:

S&P 500: Support 6,300 | Resistance 6,400 | Target 6,500

EUR/USD: Support 1.1550 | Resistance 1.1650

Gold: Support $3,300 | All-Time High $3,350+

Position Sizing: Volatility is moderate; standard risk sizing is appropriate, but consider reducing exposure ahead of Powell’s speech.

📅 Today’s Key Events

10:00 AM EST: Jackson Hole Symposium – Fed Chair Powell’s speech

Throughout the day: Monitor reactions in US and global markets, especially in rates, USD, and equities

Key Finding: The market is cautiously optimistic, with Asia leading gains and the US dollar strengthening. However, the outcome of the Jackson Hole symposium could quickly shift sentiment. Stay nimble, monitor technical levels, and be prepared for increased volatility.